The major stock indexes jumped last week, looking beyond the 6.8% US Consumer Price Index (CPI) rate reported. Stripping out food and energy, the inflation rate jumped 4.9%. Don’t think anyone is looking at the lower number at this point, as higher food and energy costs can’t be avoided at this time.

For the week, the Dow rose 4.05%, the S&P 500 3.85%, the Nasdaq Composite 3.62% and the Russell 2000 Small cap index 2.45%.

Over the pond, foreign stocks climbed 2.44% and Emerging Market Equities rising 1.15%.

Bond yields moved north, however are staying resilient, with the 10-year yield finishing last week @ 1.49%. The US Treasury 2–10-year slope that we discuss, now sits @ .83%. That slope started the year @ .79%, increased to 1.24% on September 30, 2021. Certainly, worth paying close attention to the movement of all US Treasury securities at this point.

Required Minimum Distribution (RMD) Tables Changed

This is good news for most people with retirement accounts. Beginning in 2022, you’ll notice the tables have been changed, lowering the minimum amount you need to withdraw annually from your various retirement accounts. The new tables reflect longer life expectancies.

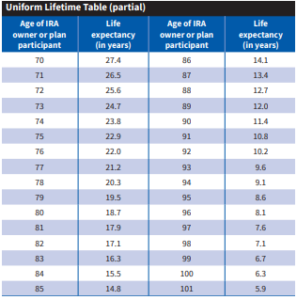

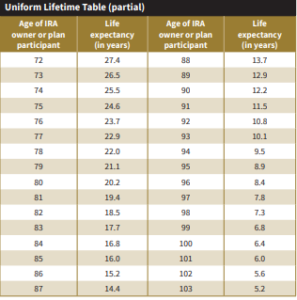

Example: Assume an IRA holder with an account balance on 12/31/2021 of $1,000,000. Let’s assume this IRA holder will turn 75 sometime in 2022. Here’s the difference in the requirement:

- Old Table: $1,000,000 divided by the old factor of 22.9 equals a minimum withdrawal of $43,668.12 to satisfy the requirement

- New Tables: $1,000,000 divided by the new factor of 24.6 equals a minimum withdrawal of $40,650.40 to satisfy the requirement.

- The difference is $3,017.72 less that needs to be withdrawn (or 6.9%).

Example #2: Assume an IRA holder with an account balance on 12/31/2021 of $1,000,000. Let’s assume this IRA holder will turn 72 sometime in 2022, and elects to take their first-year distribution in 2022, and not postpone to take 2 the following year.

- Old Tables: $1,000,000 divided by 25.6 equals $39,062.50 to meet the requirement.

- New Tables: $1,000,000 divided by 27.4 equals $36,496.35 to meet the requirement

- The difference is $2,566.15 less that needs to be withdrawn (or 6.56%).

Calculating and Keeping track of your annual RMD requirement is extremely important to avoid any unnecessary IRS penalties. We have extensive experience in this area. If you have one IRA, the calculation and choice is straight-forward. When you have multiple IRA accounts and/or 401K’s and 403B’s, you must be aware of the aggregation rules.

Annually, we field several questions finding many taxpayers have uncertainty knowing if they are truly satisfying the RMD requirements.

For clients, we track RMD’s very closely and have separate files for each client, showing each year’s calculations and withdrawals.

For nonclients with questions, please feel free to schedule a consultation to discuss your requirements, as well as see how you can use Qualified Charitable Contributions to further reduce your Income Tax situation.

Below are the two tables for you to compare your factors. The old table is on the left in blue, and the new table that will be used in 2022 is on the right, in gold.

OLD (2021) Lifetime Table: NEW (2022) Lifetime Table: